Global Veterinary Diagnostics Market Statistics: USD 13.0 Billion Value by 2033

Summary:

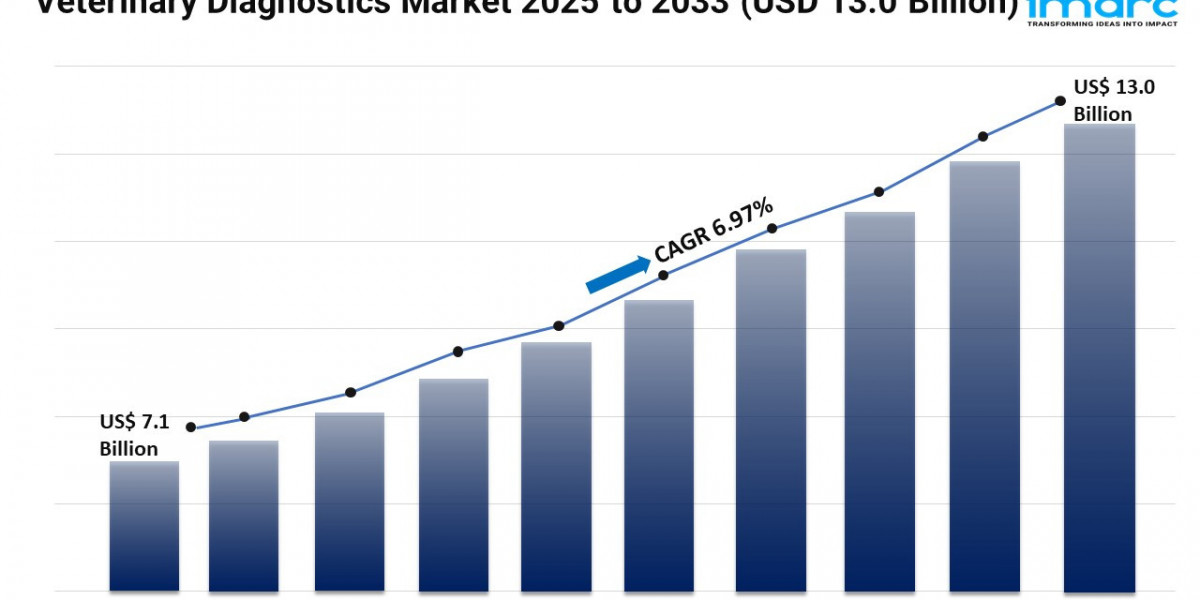

- The global veterinary diagnostics market size reached USD 7.1 Billion in 2024.

- The market is expected to reach USD 13.0 Billion by 2033, exhibiting a growth rate (CAGR) of 6.97% during 2025-2033.

- North America leads the market, accounting for the largest veterinary diagnostics market share.

- Kits and reagents account for the majority of the market share in the product segment due to their convenience and ease of use.

- Clinical biochemistry holds the largest share in the veterinary diagnostics industry.

- Livestock animals remain a dominant segment in the market as they require regular health monitoring to ensure food safety and optimize production yields.

- Non-infectious diseases represent the leading disease type segment.

- Reference laboratories account for the majority of the market share in the end user segment.

- The growing emphasis on proactive animal health monitoring is a primary driver of the veterinary diagnostics market.

- Innovations in diagnostic technology and the rising awareness about zoonotic diseases are reshaping the veterinary diagnostics market.

Industry Trends and Drivers:

- Rising demand for animal health monitoring:

A shift towards proactive animal health monitoring represents one of the key factors propelling the growth of the market. Pet parents and livestock producers are becoming more conscious about the health and well-being of their animals, which is prompting them to seek regular health check-ups and diagnostic tests. This trend is particularly evident in the pet care sector, where owners are prioritizing preventive healthcare to detect diseases early and improve the quality of life of their pets. As a result, veterinary clinics and practitioners are expanding their diagnostic capabilities to meet this rising demand. Manufacturers are innovating and developing innovative diagnostic kits and reagents facilitating quick and accurate testing, thereby supporting the market growth.

- Advancements in diagnostic technology:

New technologies, such as point-of-care (POC) testing, molecular diagnostics, and digital imaging, are enhancing the speed and accuracy of disease detection in animals. These innovations are enabling veterinarians to conduct tests efficiently, leading to quicker diagnoses and more effective treatment plans. As technology are advancing, manufacturers are introducing sophisticated equipment and testing solutions that cater to diverse diagnostic needs. This ongoing development is improving the quality of veterinary care and increasing the adoption of advanced diagnostic methods in practices worldwide. As a result, more clinics are integrating these cutting-edge technologies into their operations as a proactive approach to animal health management and disease prevention, thereby offering a favorable market outlook.

- Increasing awareness about zoonotic diseases:

The growing awareness among the masses about zoonotic diseases is positively influencing the market. As public health officials and the general population are getting more informed about the potential transmission of diseases from animals to humans, the need for effective disease monitoring and management is becoming more critical. This is encouraging veterinary professionals to implement comprehensive diagnostic testing for companion and livestock animals to prevent outbreaks and safeguard public health. In addition, regulatory bodies are emphasizing the significance of surveillance and reporting systems, which is driving the demand for reliable diagnostic tools. Manufacturers are responding by developing targeted diagnostic solutions that help identify and monitor zoonotic pathogens, thereby contributing to the growth of the market.

Request for a sample copy of this report: https://www.imarcgroup.com/veterinary-diagnostics-market/requestsample

Veterinary Diagnostics Market Report Segmentation:

Breakup By Product:

- Instruments

- Kits and Reagents

- Software and Services

Kits and reagents represent the largest segment due to their essential role in facilitating accurate and timely testing for various diseases in animals.

Breakup By Technology:

- Immunodiagnostics

- Clinical Biochemistry

- Molecular Diagnostics

- Hematology

- Others

Clinical biochemistry accounts for the majority of the market share because it provides critical information about the metabolic and physiological status of animals.

Breakup By Animal Type:

- Companion Animals

- Dogs

- Cats

- Others

- Livestock Animals

- Cattle

- Swine

- Poultry

- Others

Livestock animals exhibit clear dominance in the market, driven by the high economic value of these animals and the significant focus on their health and productivity in agricultural practices.

Breakup By Disease Type:

- Infectious Diseases

- Non-infectious Diseases

- Hereditary, Congenital and Acquired Diseases

- General Ailments

- Structural and Functional Diseases

Non-infectious diseases hold the biggest market share as they encompass a wide range of conditions, including metabolic and hereditary disorders.

Breakup By End User:

- Reference Laboratories

- Veterinary Hospitals and Clinics

- Others

Reference laboratories dominate the market owing to their advanced technology and expertise.

Breakup By Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position in the veterinary diagnostics market, which can be attributed to its thriving healthcare infrastructure, increasing investments in veterinary research, and the rising demand for advanced diagnostic technologies.

Top Veterinary Diagnostics Market Leaders:

The veterinary diagnostics market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies. Some of the key players in the market are:

- BioChek B.V.

- Biomérieux SA

- Heska Corporation

- IDvet

- IDEXX Laboratories Inc.

- Neogen Corporation

- Randox Laboratories Ltd.

- Thermo Fisher Scientific Inc.

- Virbac

- Zoetis Inc.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1–631–791–1145